Municipal triple-A benchmarks firmed Friday after a less-than-stellar employment report while a lackluster new-issue calendar awaits investors, with strong underlying technicals keeping rates low.

Volume is estimated at $6.569 billion for the week of May 10, up from total sales of $1.840 billion the week of May 3. The supply-demand imbalance, solid fund inflows and the improving credit environment themes remain the same heading into the second week of May and do not appear to be abating.

"We see rather smooth sailing for our asset class over the summer months, with only rate volatility possibly throwing a wrench in the works (although the probability of a large rate sell-off near term has probably declined somewhat after [Friday's] payrolls)," Barclays PLC strategists wrote in a Friday report.

Aside from possible rate volatility, it is "hard to be overly bearish on tax-exempts, although valuations are getting squeezed and spreads continue to grind tighter, keeping many investors on the sidelines," Barclays strategists Mikhail Foux, Clare Pickering and Mayur Patel wrote.

Triple-A benchmarks fell one to two basis points across the curve while municipal to UST ratios closed at 63% in 10 years and 70% in 30 years on Friday, according to Refinitiv MMD, while ICE Data Services had the 10-year at 62% and the 30 at 71%.

While trading activity dipped again in April, despite record inflows and cash cushions helped by mutual funds, supply also ended up well below investor expectations last month, and the typically heavy May also started quite slowly, with the 30-day visible supply at its lowest point since late March, they said. And while summer redemptions are just around the corner, creating a positive backdrop, especially for the most actively traded states, such as New York and California, they do expect net issuance over the next 30 days in Washington and Texas to be positive.

There are $4.997 billion of municipal bond sales scheduled for negotiated sale versus a revised $617.1 million this week. Bonds scheduled for competitive sale total $1.517 billion compared with $1.223 billion this week.

As for credits, the largest deal comes from Washington State's Energy Northwest with $1.1 billion of exempt and taxables, while the Main Street Natural Gas, Inc. (Aa2//AA/) is still on the day-to-day calendar, with $747.1 million of gas supply revenue bonds led by RBC Capital Markets Inc. The Dormitory Authority of the State of New York is bringing various-rated credits worth $461 million, including $125.9 of St. John's University revenue bonds. Gilt-edged Fairfax County, Virginia, will price $232 million of sewer bonds and the largest competitive loan comes out of New Mexico: $171.7 million of capital projects general obligation bonds selling Wednesday.

Inflation is clearly a focus for all markets, with breakevens trending higher and getting close to their early-2018 levels, while Treasury yields are still more than 100 basis points below their 2018 yields, "possibly leaving room for a negative surprise this summer, with likely spillover effects into munis, although it is absolutely not a given that rates will come under pressure," according to the report.

"If rates are stuck in a narrow range over the next several months, munis will likely move sideways, with a slight positive bias on prices and spreads," the report said. "However, it is hard to expect much price appreciation at current levels, especially in high grade, and investors will most likely be left to clip coupons for the time being."

Scales

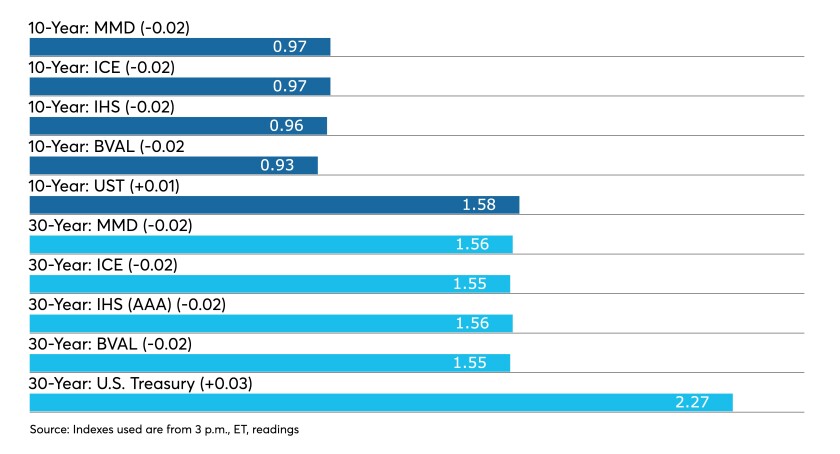

On Refinitiv MMD’s AAA benchmark scale, yields were steady at 0.09% in 2022 and 0.12% in 2023. The yield on the 10-year fell one basis point to 0.98% as did the 30-year to 1.57%.

The ICE AAA municipal yield curve showed yields at 0.09% in 2022 and 0.13% in 2023, the 10-year fell two to 0.97%, while the 30-year fell to 1.55%.

The IHS Markit municipal analytics AAA curve showed yields fell one basis point to 0.09% in 2022 and 0.12% in 2023, the 10-year fell two to 0.96% and the 30-year fell two to 1.56%.

The Bloomberg BVAL AAA curve showed yields fell one basis point to 0.05% in 2022 and 0.07% in 2023, with the 10-year down two to 0.93%, and the 30-year yield down two basis points to 1.55%.

The three-month Treasury note was yielding 0.02%, the 10-year Treasury was yielding 1.58% and the 30-year Treasury was yielding 2.27% near the close. Equities were stronger to end the week with the Dow gaining 237 points, the S&P 500 rising 0.82% and the Nasdaq up 1.02% near the close.

One for the Fed

A disappointing jobs report gives credence to the Federal Reserve’s concern about the slack in the labor market.

Nonfarm payrolls grew by 266,000 in April, when estimates suggested growth of a million jobs. The unemployment rate ticked up to 6.1%, when economists expected it to decline to 5.7%.

“This is an incredibly disappointing economic data point and supports the Federal Reserve’s concern over employment,” said Bryce Doty, senior vice president and senior portfolio manager at Sit Fixed Income. “However, the economy is rebounding so strongly, the recovery in jobs is a matter of when and not if it will happen.”

“From the market’s perspective, this morning’s weaker-than-expected rise in payrolls coupled with a backup in the unemployment rate will call into question the momentum of the recovery,” said Stifel Chief Economist Lindsey Piegza.

But the report wasn’t all bad, according to Christian Scherrmann, U.S. Economist at DWS. “Leisure & hospitality actually posted more new jobs than in March, at 331k,” he said. “This could well serve as an indication that demand is returning to the sector that was hit hardest by the pandemic.”

Other positives were the labor participation rate climbing 0.2-points to 61.7% in April and fewer part-time employees, as their hours were increased, perhaps to meet rising demand, Scherrmann said.

“Euphoria about a very quick recovery in the labor market might have been somewhat overdone,” he added. “And yet the marked fall in part-time jobs suggests the quality of employment is improving and gives grounds for some optimism looking ahead.”

Doty said the miss this month will likely lead to “a blowout number to the upside.”

“Finding a convincing theme” in the report is “challenging,” said Marvin Loh, senior global macro strategist at State Street. He pointed to the rise in hourly earnings, which was fueled by “lower wage industries in the leisure and entertainment sectors.”

“The question now emerges as to whether the economy is decelerating into the current quarter or whether this one jobs report is just a hiccup in the long recovery road,” Loh said.

The Fed said there needs to be “a string of positive reports before it considers normalizing policy,” he said. “This report clearly does not fit the narrative, and talk of tapering remains premature. The market timing of the first rate hike (early 2023) will also appear aggressive unless we start to see a more rapid recovery in the employment over the summer. If anything, this jobs report shows that road to recovery, like overcoming the pandemic, will be bumpy and include surprises.”

Scott Ruesterholz, portfolio manager at Insight Investment said, “The soft headline number should enable the Federal Reserve to push out any market speculation on tapering a bit longer.”

While the report shows a “reopening boost, Brian Coulton, chief economist at Fitch Ratings said, the increased jobless rate and the downward revision to new March jobs (to a rise of 770,000 from the initially reported 916,000) “emphasize just how far away we still are from regaining full employment."

Noting that it is only one read, Sameer Samana, senior global market strategist at Wells Fargo Investment Institute, said “[we] continue to think the labor market remains on track and will be more than enough to underpin consumer confidence and consumption.”

Ruesterholz noted, “In the one year since the COVID-19 recession began, we have made as much progress as it took us in the seven years after the financial crisis.”

And while the initial “policy response … seemed extraordinary at the time,” he said, it “may become normal during future recessions.”

Also released Friday, wholesale inventories grew 1.3% in March, following a downwardly revised 1.0% gain in February, initially reported as a 1.4% gain, while wholesales sales gained 4.6% after an upwardly revised flat reading the prior month, first reported as a 0.8% decline.

Economists anticipated inventories would increase 1.4% in the month.

Primary to come

The Main Street Natural Gas, Inc. (Aa2//AA/) is on the day-to-day calendar with $747.1 million of gas supply revenue bonds, serials 2022-2028, a term in 2051, puts due 12/1/2028. RBC Capital Markets Inc. is lead underwriter.

Energy Northwest in Washington state (Aa2/AA-/AA/) is expected to price on Tuesday $1.1 billion of exampts and taxables, comprised of $68.7 million of Project 1 electric revenue refunding bonds, Series 2021-A, $523.97 million of Columbia Generating Station electric revenue and refunding bonds, Series 2021-A, $15.4 million of Project 3 electric revenue refunding bonds, Series 2021-A, $395 million of taxable Project 1 electric revenue refunding bonds, Series 2021-B, and $100.8 million of taxable Columbia Generating Station electric revenue refunding bonds, Series 2021-B. J.P. Morgan Securities LLC is set to run the books.

The Dormitory Authority of the State of New York is set to price on Tuesday $336.3 million of school district revenue bond financing program refunding bonds Series 2021A, B & C, consisting of $277.2 million Series 2021A (A1//AA-/), serials 2022-2041, term, 2046, 2050; $47.27 million of Series 2021B (Aa3//AA-/), serials 2022-2041, terms, 2046, 2050; and $11.87 million of Series 2021C (A1//AA-), serials 2022-2035. Raymond James & Associates, Inc. is lead underwriter.

DASNY (Aa3/A-//) is also set to price $125.9 million of St. John’s University revenue bonds Series 2021A on Wednesday. Morgan Stanley & Co. LLC is head underwriter.

Rady Children’s Hospital in San Diego (Aa3//AA/) is set to price $300 million of taxable corporate CUSIP Series 2021A bonds. J.P. Morgan Securities LLC is head underwriter.

The San Antonio Independent School District, Bexar County, Texas, (Aaa//AAA/) is set to price $254.2 million of unlimited tax school building bonds, Series 2021, insured by Permanent School Fund Guarantee Program. Morgan Stanley & Co. LLC is bookrunner.

Fairfax County, Virginia, (Aaa/AAA/AAA/) is set to price on Tuesday $232 million of sewer revenue bonds, Series 2021A and sewer revenue refunding bonds. Morgan Stanley & Co. LLC is head underwriter.

Johnson County, Kansas, (Aaa///) is set to price $157.7 million of Shawnee Mission Unified School District Number 512 general obligation refunding and improvement bonds. Stifel, Nicolaus & Company, Inc. is lead underwriter.

The Central Valley Water Reclamation Facility (/AA/AA/) is expected to price $150.4 million of sewer revenue green bonds on Tuesday. Stifel, Nicolaus is bookrunner.

The North Dakota Housing Finance Agency (Aa1///) is set to price on Wednesday $120 million of housing finance program home mortgage finance program bonds, serials 2022-2033, terms 2036, 2041, 2044, 2052. RBC Capital Markets is bookrunner.

Grand Forks, North Dakota, is set to price $118 million of Solid Waste Disposal Facility Revenue Bonds (Red River Biorefinery, LLC Project), Series 2021A (Green Bonds), Series 2021B refunding green bonds (Turbo Bonds). Jefferies LLC is head underwriter.

The Erie County, New York, Industrial Development Agency (Aa3/AA//) is set to price on Wednesday $110.1 million of school facility refunding revenue bonds (City School District of the City of Buffalo Project), Series 2021A school facility refunding revenue bonds and Series 2021B school facility refunding revenue bonds. Citigroup Global Markets Inc. will run the books.

The Fremont Union High School District, Santa Clara County, California, (Aaa/AAA//) is set to price on Tuesday $110 million of general obligation green bonds. Morgan Stanley & Co. LLC is head underwriter.

Fremont UHSD is also set to price on Tuesday $101.5 million of taxable general obligation refunding bonds. Morgan Stanley is set to run the books.

The Higher Education Student Assistance Authority, New Jersey, is set to price on Tuesday $108.56 million of student loan revenue and refunding bonds consisting of $11.48 million Series A-SEN (/AA//), serials 2023-2029; $84.08 million Series B-SEN, serials 2023-2029, term 2040 (/AA//) and $13 million Series C-SUB (/BBB//) serial 2051. RBC Capital Markets will run the books.

The Huntington Beach Union High School District, Orange County, California, (/AA-//) is set to price on Wednesday $104 million of taxable general obligation refunding bonds. Wells Fargo Securities is lead underwriter.

The Rhode Island Health and Educational Building Corp. (Aa3///) is set to price $100.7 million of public school revenue bond financing program revenue bonds, Series 2021 D (City of Providence Issue), serials 2024-2041. Raymond James & Associates, Inc. is head underwriter.

Grossmont-Cuyamaca Community College District, San Diego County, California, (Aa2/AA//) is set to price on Tuesday $100 million of general obligation bonds, Election of 2012, Series 2021, serials 2030-2041, terms 2046, 2050. Stifel, Nicolaus & Company, Inc. is bookrunner.

The Florida Development Finance Corp. is set to price on Tuesday $89.27 million of senior living revenue and refunding bonds (The Glenridge on Palmer Ranch Project) Series 2021. Piper Sandler & Co. is head underwriter.

Competitive slate

On Tuesday, Hillsborough County, Florida, (Aa1/AAA/AA+/)) is set to sell $164 million of capital improvement non-ad valorem tax revenue bonds at 10:30 a.m. eastern.

Portland, Oregon, (/AA//)) is set to sell $163 million of senior lien water system revenue and refund bonds Series 2021 at 11 a.m.

On Wednesday, New Mexico (Aa2/AA//) is set to sell $171.7 million of capital projects general obligation bonds at 10:30 a.m. eastern.

"low" - Google News

May 08, 2021 at 02:58AM

https://ift.tt/3vV9mk7

Another week of sub-par volume to keep rates low - Bond Buyer

"low" - Google News

https://ift.tt/2z1WHDx

Bagikan Berita Ini

0 Response to "Another week of sub-par volume to keep rates low - Bond Buyer"

Post a Comment